What a difference six months can make. With inflation and interest rates falling, wage pressures easing and efforts to reduce staff turnover paying dividends, most property businesses have found themselves fairing much better in the final months of 2025 than they were back in March.

A series of interest rate cuts and inflation stabilising within the Reserve Bank’s target 2-3% band have seen consumer confidence and homebuyer demand rebound, while a cooling labour market has taken some of the pressure off employers.

It may not feel like it for those battling continued operational challenges on an everyday basis, but a collective overview shows that the property industry appears to have turned a corner in 2025. And many businesses are now forecasting a positive year ahead.

Nevertheless, skills shortages and wage pressures continue to persist, while regulatory changes are throwing up new challenges and impacting upon working conditions across the industry.

Taking advantage of more favourable economic and labour conditions demands a solid understanding of the prevailing remuneration expectations within each sector and across the wider industry.

The latest Avdiev Insights Survey report for October 2025 offers property businesses a comprehensive, real-time overview of the current remuneration landscape, as well as a timely opportunity to compare their own performance, policies and budgetary frameworks to those of their industry peers. We have included a snapshot of the results below. Order your copy today for the full results.

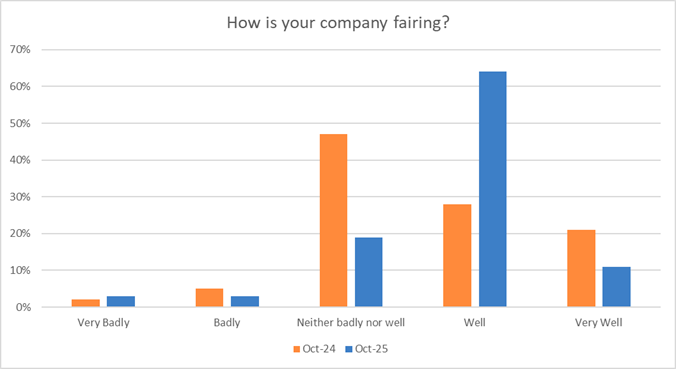

Dramatic turnaround in business performance

All sectors of the property industry recorded an upswing in business performance this year, with 75% of respondents stating their business is currently performing “well” or “very well”, as a combination of factors unite to bring about more normal trading conditions.

This marks a significant turnaround in just six months, with only 49% of respondents stating the same in our March 2025 survey.

The change was most pronounced among Real Estate Agency and Advisory firms, where there was a concentration of businesses performing poorly in March 2025, but this is now one of the best performing sectors.

Just 3% of respondents said their company is doing “badly” and a similar proportion reported doing “very badly”. The remainder were neither optimistic nor pessimistic about their performance.

There is an even split across sectors in their expectations for what lies ahead in 2026, with four anticipating even better performance while the remaining four believe the next 12 months will bring much the same. No sectors foresee a worsening in their performance.

Remuneration continues to moderate

While the Reserve Bank notes that quarterly CPI has been contained below 3% for the past year, many sectors of the property industry have continued to see remuneration increases well above this level.

Between 70% and 85% of staff were given the usual full increase, with a minimal increase given to between 5% and 20% of staff. There was considerable spread in these increases, both across individual sectors and staff seniority levels, of between 1.0% and 8.0%.

However, the higher percentage increases tended to be reserved for junior and mid-level staff, and 30% of companies attributed higher remuneration increases to catch-up rises.

Companies are forecasting much more moderate increases over the year ahead, averaging 3.4% for both senior and mid-level staff and 3.6% for junior staff. This is down from the expected 4% average increase recorded six months ago.

Retention strategies showing positive results

The skills shortages of recent years have seen employers aggressively target retention strategies in a bid to avoid turnover exacerbating key skills gaps. And our latest survey shows these strategies appear to be paying off.

Staff turnover across the property industry fell by 45% over the past year, with voluntary turnover plummeting by 53%. In fact, 30% of companies said they had no employees leave their ranks within the past 12 months.

This has helped the majority of property business to grow their staffing levels over the year.

Managers in short supply

Skills shortages and recruitment difficulties remain a headache across the industry. These gaps are being predominantly felt in manager-level roles, in positions as diverse as technology, finance and accounting, and project management.

It comes a time when a raft of regulatory and company policy changes – including Right to disconnect legislation, psychosocial hazards and expanded Paid Parental Leave – are impacting on working conditions, with fewer managers available to led teams through the changes.

Given just 13.33% of companies said their ability to recruit was better than 12 months ago, many are increasingly looking to expand their training and development programs in order to fill key gaps and promote from within their existing ranks. While no quick fix to the skills shortages experienced in the present day, given the substantial time and capital investments involved, how this approach plays out over the longer term will form a key focus of future surveys.